Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Friday Fun Facts – The Average American Moves 12 Times in Their Life

According to the U.S. Census Bureau, the average American moves approximately 11.7 times throughout their lifetime. However, this number varies widely depending on factors such as age, income, and marital status.

Young adults between the ages of 18 and 34 move much more frequently than older adults. Folks between 18 and 34 have an average of 3.3 moves under their belts. In contrast, adults aged 65 and over move much less frequently, with an average of 2.4 moves throughout their lifetime.

Times have changed. While Americans used to move for job opportunities, most people nowadays choose to move for personal reasons. Being closer to families and seeking a better quality of life have become major driving forces behind American relocations.

Of course, the COVID-19 pandemic has also had a significant impact on American mobility. Many people took the chance to re-evaluate their living situations in light of remote work and other changes in the workplace. After all, if you’re going to work from home, why not make your home someplace nice?

Sources: U.S. Census Bureau and MovingFeedback.com

What Gives?

“I thought the market was cooling off, so why are prices still going up?”

This is a frequent question we hear from our clients.

They are understandably confused by the fact that average prices have continued to rise at a rapid pace even though sales activity is slower than what it was 6 months ago.

Bottom line, they want to know why prices are up along the Front Range anywhere from 12% to 17% compared to last year.

Firstly, we don’t expect this pace of price appreciation to continue. What we foresee is price growth going back to the long term average of 5% to 6% per year.

The reason why we still see double-digit growth comes down to two words. Supply and Demand.

Supply, while higher than a year ago, is still relatively low.

Also demand, while lower than a year ago, is still relatively high.

The market is still healthy, just not as frantic as it was.

Properties are still selling, but bidding wars and multiple offers have mostly gone away.

Sellers remain in a strong position, but they face more competition than before.

War and Interest Rates

Our clients are curious to know what the conflict in the Ukraine will mean for mortgage rates.

The short answer is down in the near term and up in the long term.

Generally speaking, economic and political uncertainty drive people to invest in bonds rather than stocks, which puts downward pressure on interest rates.

So, in the near term, the conflict in the Ukraine will push rates down slightly. We have already seen this happen as 30-year rates have dipped in the last few days.

The conflict is likely to push oil prices up which means higher gasoline prices. This will cause upward pressure on inflation, which ultimately causes upward pressure on interest rates.

So, the longer the war lasts in Europe, the more likely it is to push interest rates even higher.

Zillow’s Shut Down

On Wednesday Zillow announced the shut down of its iBuying program because of mounting financial losses and increasing complexity in the real estate market.

The goal of this program was to buy properties directly from Sellers and then re-sell them for a profit.

Before looking at the interesting facts and numbers associated with this news, we want to acknowledge the people who are affected by this.

Zillow’s workforce will be reduced by 25%. Many people will be laid off and our heart goes out to them. We certainly wish them only the best.

Within our company we are not surprised by Zillow’s announcement. We observed many cases where they over-paid for a property, re-listed it for an unrealistic price, dropped the price over time to meet the market, and then sold at an amount much less than what they paid.

It actually became difficult to find specific scenarios where they sold the home for more than their acquisition cost. It was not uncommon to see losses of $50,000 per home or more.

Here is a quote from their CEO: “Our observed error rate has been far more volatile than we thought possible. Fundamentally, we have been unable to predict future pricing of homes to a level of accuracy that makes this a safe business to be in.“

In the third quarter of 2021 alone, their iBuying division lost $328 million.

Bottom line, their valuations were off.

It is a reminder that pricing requires a hyper-local scientific approach versus a generic algorithm

Homes are not commodities. Each home is highly unique. Each has its own highly unique location, features, amenities, condition and timing.

Homes can’t be priced like a book or a plane ticket. Every unique feature must be taken into account.

Nationally, Zillow has about 7,000 homes in backlog which it hopes to sell over the next several months.

Other players remain in the iBuying game and we are more than happy to help you understand those options if you are curious.

Words Matter

A common phrase that is being used right now to describe the market is ‘no inventory.’

‘There’s no inventory’ is said frequently among those inside and outside of the real estate industry.

The problem with this phrase is that it is untrue.

There is inventory. Meaning, there are a significant number of new listings hitting the market.

However, there is low standing inventory. Meaning, the listings that do hit the market don’t stick around for very long before they are purchased.

Standing inventory, which is the number of active properties on the market, is down roughly 70% along the Front Range.

However, the number of new listings coming on the market is essentially:

- Double compared to December 2020

- Only 20% to 25% less than this time of year in 2017, 2018, and 2019

So, there is inventory available, it just sells quickly because demand is historically high right now.

Q1 2021 Colorado Real Estate Market Update

The following analysis of the Metro Denver & Northern Colorado real estate market is provided by Windermere Real Estate Chief Economist Matthew Gardner. We hope that this information may assist you with making better-informed real estate decisions. For further information about the housing market in your area, please don’t hesitate to contact your Windermere Real Estate agent.

REGIONAL ECONOMIC OVERVIEW

Following the decline in employment last winter, Colorado has started to add jobs back into its economy. The latest data shows that the state has now recovered more than 219,000 of the 376,000+ jobs that were lost due to COVID-19. This is certainly positive, but there is a long way to go to get back to pre-pandemic employment levels. Denver and Fort Collins continue to have the greatest improvement in employment, but all markets show job levels well below pre-pandemic levels. With total employment levels rising, the unemployment rate stands at 6.6%, down from the pandemic peak of 12.1%. Regionally, unemployment levels range from a low of 5.6% in Fort Collins and Boulder to a high of 6.7% in Greeley. COVID-19 infection rates have started to increase again, and this has the potential to negatively impact the job market. I am hopeful that the state will not be forced to pull back reopening, but this is certainly not assured.

COLORADO HOME SALES

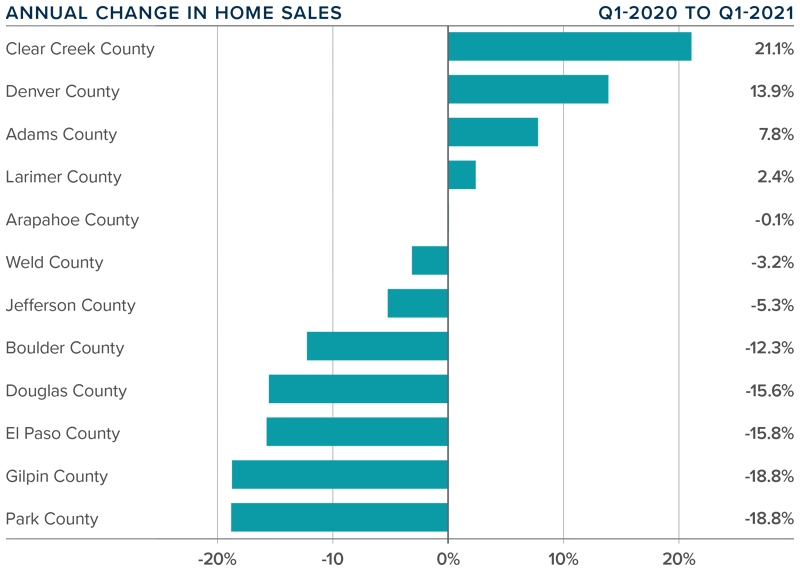

❱ 2021 started off on a bit of a sour note, with total sales down 1.2% compared to the same period in 2020. Sales were 29.2% lower than in the final quarter of 2020 as 8,645 homes sold.

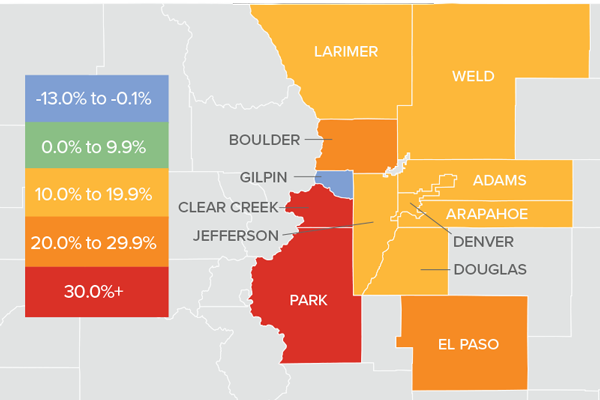

❱ Sales were higher in four of the counties contained in this report, were essentially flat in one, and dropped in seven. It was pleasing to see significant sales growth in the large counties of Denver and Adams.

❱ Another positive was that pending sales, which are an indicator of future closings, were 4.8% higher than in the fourth quarter of 2020 and 5% higher than a year ago.

❱ The disappointing number of home sales overall can primarily be attributed to the woeful lack of inventory. Listings in the quarter were down more than 61% year over year and were 40.6% lower than in the fourth quarter of 2020.

COLORADO HOME PRICES

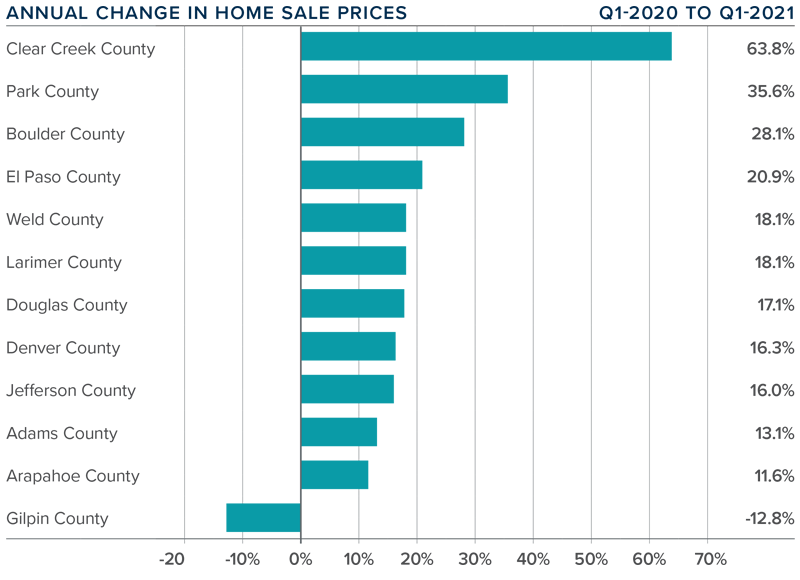

❱ Prices continue to appreciate at a very rapid pace, with the average sale price up 16.5% year over year, to an average of $556,100. Home prices were also 4.4% higher than in the fourth quarter of 2020.

❱ Buyers appear to be out in force, and this demand—in concert with very low levels of inventory—continues to heat the market.

❱ Prices rose over last year across all markets covered by this report, with the exception of the very small Gilpin County. All other counties saw sizeable gains and the trend of double-digit price growth continued unabated.

❱ Affordability levels are becoming a greater concern as prices rise at a far faster pace than wages. Even though mortgage rates have started to rise, they haven’t yet reached the level needed to take some of the heat out of the market.

DAYS ON MARKET

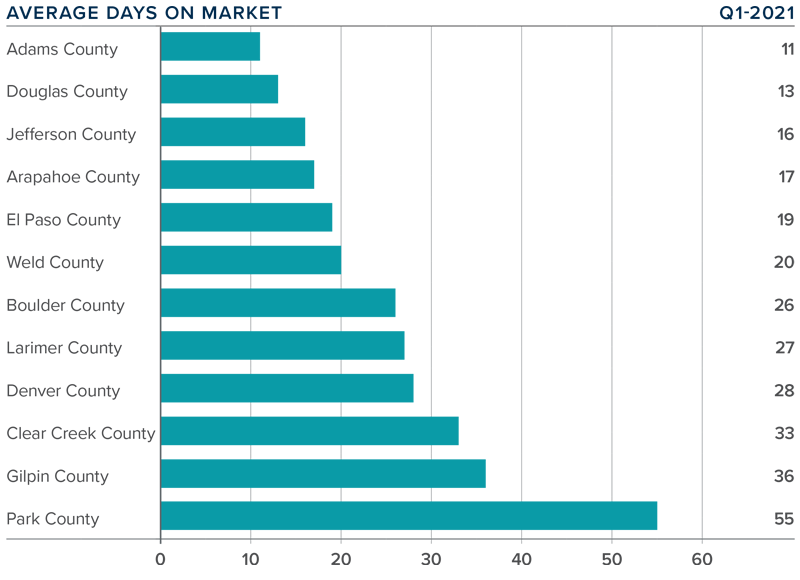

❱ The average time it took to sell a home in the markets contained in this report dropped 20 days compared to the first quarter of 2020.

❱ The amount of time it took to sell a home dropped in every county contained in this report compared to the fourth quarter of 2020.

❱ It took an average of 25 days to sell a home in the region, down one day from the fourth quarter of 2020.

❱ The Colorado housing market remains very tight, as demonstrated by the fact that it took less than a month for homes to sell in all but two counties.

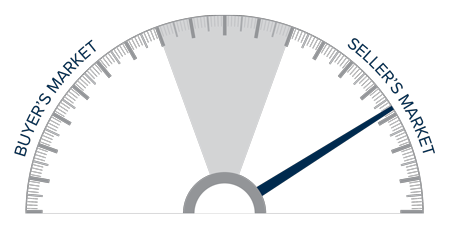

CONCLUSIONS

This speedometer reflects the state of the region’s real estate market using housing inventory, price gains, home sales, interest rates, and larger economic factors.

The relatively low level of home sales is not a surprise given how few choices there are for buyers. Sellers are certainly benefitting from strong demand, as demonstrated by the significant price growth. I maintain my belief that there will be an increase in inventory as we move through the year, but it is highly unlikely that we will see a balanced market in 2021.

Given these factors, I am moving the needle a little more in favor of sellers, as demand is likely to continue to exceed supply.

ABOUT MATTHEW GARDNER

As Chief Economist for Windermere Real Estate, Matthew Gardner is responsible for analyzing and interpreting economic data and its impact on the real estate market on both a local and national level. Matthew has over 30 years of professional experience both in the U.S. and U.K.

In addition to his day-to-day responsibilities, Matthew sits on the Washington State Governors Council of Economic Advisors; chairs the Board of Trustees at the Washington Center for Real Estate Research at the University of Washington; and is an Advisory Board Member at the Runstad Center for Real Estate Studies at the University of Washington where he also lectures in real estate economics.

Economic Update with Matthew Gardner

Exclusive Invitation!!!

Tune in on Tuesday, October 6, 2020 at 9:00am to meet with Matthew Gardner, Windermere Real Estate’s Chief Economist LIVE and get your chance to ask him questions. He’ll be discussing the housing market, employment and the effects of COVID-19 on the local and national economy.

As one of the only real estate companies in the US that has a Chief Economist on staff, we have exclusive insights into the housing market, economy and government happenings. This is a one of a kind event for clients and friends of Windermere Real Estate in Colorado.

To sign up, please contact your Windermere Agent or message us to get the link. Seating is limited in digital meeting room so get your seat!

(If you can’t attend live, you can register to automatically get the recording.)

Matthew Gardner’s 2020 Real Estate Forecast

It’s that time of year when Windermere’s Chief Economist Matthew Gardner dusts off his crystal ball and peers into the future to give us his predictions for the 2020 economy and housing market.

Our Favorite Real Estate Podcasts

Podcasts are a growing medium as listeners search for new sources of entertainment and information. In 2018 there were about 550,000 podcasts, in 2019 there are more than 750,000. Listeners are growing too, an estimated 20 million more people in the U.S. are listening to podcasts this year as compared to2018.

This growth in audio entertainment inspired us to pull together a few of our favorite real estate podcasts. Whether you’re interested in investing in real estate, looking to make a move to a new home, or just want to know what’s happening in the market, here are our recommendations:

For Investors:

The Millennial Real Estate Investor

Find your niches in Real Estate with Dan Mackin and Ben Welch, who host experts with stories about their investing successes and challenges. Learn from the experienced guests on this show the many ways to get into investing and succeed at it.

Listen to Millennial Real Estate Investor wherever you get your podcasts (Icon linked):

![]()

Cash Flow Connection

If you’re drawn to the commercial side of real estate, Cash Flow Connections with host, Hunter Thompson, is an informative podcast that interviews leading investors, sponsors and managers. Learn about all the aspects of commercial real estate from all viewpoints to find the right fit for you.

Windermere’s Chief Economist, Matthew Gardner, was just interviewed about the state of the real estate market, and what to expect in the next recession (hint: it won’t be driven by housing). You can listen to that episode here.

Listen to Cash Flow Connection wherever you get your podcasts:

![]()

For Those About to Move

Windermere Home and Wealth

Host Brian Bushlach interviews business owners, local guides, and Windermere agents in each episode about different areas throughout the Western U.S. and what they have to offer to those who live or visit there. Learn about what’s attracting newcomers to the area, and what the local real estate market looks like. This podcast is sure to stir your wanderlust.

Listen to Windermere Home and Wealth wherever you get your podcasts:

![]()

Finding Home with 106.1 KISS FM

Join first-time home buyers, and radio personalities, Anthony and Carla Marie from 106.1 KISS FM, as they walk through the home buying journey with their Windermere agents. This podcast is both entertaining and informative as they ask the questions you’ve always wanted answers to. With their knowledgeable real estate agents by their sides, they’re taking you along as they get approved, look for houses, and even put an offer on a home.

Listen to Finding Home on iHeartRadio:

![]()

Stay Informed

Housing Developments

Hosted by National Association of Home Builders CEO Jerry Howard and Chief Lobbyist Jim Tobin, this podcast covers updates in the housing market and building industry across the nation. Learn from experts in the field about recent laws and the news of the industry.

Listen to Housing Developments wherever you get your podcasts:

![]()

Real Estate News with Kathy Fettke

This podcast is aimed at real estate investors who want to stay curren on the latest real estate news. Presented in bite sized episodes, listeners can learn about laws, regulations, and economic events that affect real estate and their local market.

Listen wherever you get your podcasts:

![]()

Why So Many Americans Are Either Upsizing or Downsizing

Posted in Buying, Selling, and Living by Shelley Rossi

According to two recent surveys that took industry watchers by surprise, many family homeowners are putting frugality aside and upsizing to new houses that average as large as 2,480 square feet (an increase of as much as 13 percent from the year before), and sometimes exceed 3,500 square feet in size.

Meanwhile, millions of baby boomer homeowners are rushing to downsize—with some 40 percent of Americans between the ages of 50 and 64 saying they’re planning to make a move within the next five years.

It’s a tale of two very different segments of the population making dramatic shifts in their living accommodations to find the housing solutions that best suit their needs: one upsizing while the other downsizes.

With so many baby boomers now nearing retirement age (8,000 Americans turn 65 every day), it should come as no surprise that the number of prospective “downsizers” exceed the number of “upsizers” by three to one. With their children gone, these aging homeowners are interested in reducing the amount of house they need to care for, and are eager to bulk up their retirement savings with any home-sale profits.

As for why many families are choosing to upsize so substantially after years of downsizing or staying put, experts point to the extremely low interest rates and discounted home prices available today, and theorize that many families now feel confident enough about the economy to move out of homes they outgrew years ago.

If you’re considering upsizing or downsizing, here are some facts to consider:

How such a move can impact your life

The most common benefits of downsizing:

- Lower mortgage payments

- Lower tax bills

- Lower utility bills

- Less maintenance (and lower maintenance expenses)

- More time/money for travel, hobbies, etc.

- More money to put toward retirement, debts, etc. (the profits from selling your current home)

The most common benefits of upsizing

- More living space

- More storage space

- More yard/garden space

- More room for entertaining/hosting friends and family

Negative impacts:

- Upsizing will likely increase your living expenses, so it’s important to factor into any financial forecasts

- Downsizing will require that you make some hard choices about what belongings will need to be stored or sold

Other impacts to consider:

- The loss of good neighbors

- Lifestyle changes (walking, neighborhood shopping, etc.)

- The effect on your work commute

- Public transit options

Buy first, or sell first?

Homeowners considering this transition almost always have the same initial question: “Should I buy the new home now, or wait and sell my current place first?” The answer is dependent on your personal circumstances. However, experts generally recommend selling first.

Selling your current home before buying a new one could mean you have to move to temporary quarters for some period of time—or rush to buy a new home. That could prove stressful and upsetting. However, if you instead buy first, you could be stuck with two mortgages, plus double property tax and insurance payments, which could quickly add up to lasting financial troubles.

If you need to sell in order to qualify for a loan, there’s no choice: You’ll have to sell first.

Another option:

You could make the purchase of the new house contingent on selling your current home. However, this approach can put you in a weak bargaining position with the seller (if you can even find a seller willing to seriously consider a contingency offer). Plus, you may be forced to accept a low-ball offer for your current house in order to sell it in time to meet the contingency agreement timing.

The truth is, most home sales tend to take longer than the owners imagine, so it’s almost always best to finalize the sale, and do whatever is necessary to reap the biggest profit, before embarking on the purchase of your new home.

When to make the transition

Ideally, when you’re selling your home, you want to wait until the demand from potential buyers is high (to maximize your selling price). But in this case, because you’re also buying, you’ll also want to take advantage of any discounted interest rates and reduced home prices (both of which will fade away as the demand for homes grows).

How will you know when the timing is right to both sell and buy? Ask an industry expert: your real estate agent. As someone who has their finger on the pulse of the housing market every day, they can help you evaluate the current market and try to predict what changes could be coming in the near future.

Even if you’ve been through it before, the act of upsizing or downsizing can be complex. For tips, as well as answers to any questions, contact a Windermere agent any time.