Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Friday Fun Facts – Have We Reached a Balanced Market?

Windermere Principal Economist Jeff Tucker analyzes the National Association of REALTORS’ September U.S. home sales report, what the findings say about the current housing market, and why mortgage rates have been rising in recent weeks.

Top Three

Here are the top three reasons why prices are unlikely to crash even though the market has cooled off:

- Inventory – Ultimately, prices are driven by supply and demand. Although supply has increased, it still remains relatively low with less than two months’ supply in most areas.

- New Homes – New home construction still lags behind the demand stemming from population growth. New home starts today are roughly 2/3 of what they were in 2005.

- Credit – Home buyers today are highly qualified which protects the market from a glut of ‘distressed’ properties hitting the market in an economic downturn. The average credit score of buyers is now 776 which, by definition, is ‘excellent.’ Only 2% of loans today are given to buyers with scores under 640 whereas in 2001 25% of buyers had that low of a score.

Slight Increase

A review of the September market stats shows a slight increase in inventory along the Front Range.

The way we currently measure inventory is in days.

Meaning, at the current pace of sales, how many days would it take to sell all of the inventory currently for sale.

The results, based on September’s activity, shows only a slight increase compared to August. This increase can be tied to seasonality as we always experience a slight cooling off of the market heading into the Fall.

Here is what the residential inventory looks like in each of our markets:

- Larimer County = 25 days

- Weld County = 23 days

- Metro Denver = 21 days

Bottom line, the residential market is still very healthy.

Colorado Ranking

Here’s the latest from one of our favorite data sources – the Federal Housing Finance Authority (FHFA).

They track home prices across the Country and produce a quarterly Home Price Index report.

It is not uncommon to find Colorado near the top of the list for year over year price growth.

The latest report has us ranked 13th with only a 13% year over year increase (said with sarcasm).

Idaho is first with a whopping 24% increase. Utah is second at 19%.

Here is our interpretation of these numbers…

Colorado has a history of strong, steady price growth instead of booms and busts.

Our market does not take the big, wild swings in prices that other markets sometimes do.

The fact that Colorado is not at the very top of the list right now is actually good news to us.

We know that our clients appreciate a market that is more steady instead of one that can feel like a rollercoaster.

Want a house in Fort Collins? Grab $500,000, get in line and join the housing Hunger Games

“Buying a house in Fort Collins these days can feel like a combat sport. Maybe more like the

‘Hunger Games.’ Or Charlie Brown and the football — every time you get close to the ball,

Lucy whisks it away…”

Pat Ferrier at the Fort Collins Coloradoan breaks down the housing market in Northern Colorado with the help real estate professionals across the front range. Click the link below to read on!

Fort Collins real estate_ Average home price near $500K in market

5.5 Million Short

New home construction is behind by 5.5 million homes over the last 14 years.

Since 2007, new home starts have lagged significantly behind the long-term average.

The Census Bureau started tracking National new home starts in 1958.

Between 1958 and 2007, an average of 1,102,938 new homes were started each year.

Between 2007 and 2020 the average fell to 708,186 which represents a shortfall of 394,752 per year.

That adds up to a total shortfall of 5,526,525.

The under-supply of new homes is of course a significant reason why the market is under-supplied overall.

credit Inman News as the source of this story

Colorado Real Estate Market Update

The following analysis of the Metro Denver & Northern Colorado real estate market is provided by Windermere Real Estate Chief Economist Matthew Gardner. We hope that this information may assist you with making better-informed real estate decisions. For further information about the housing market in your area, please don’t hesitate to contact your Windermere agent.

ECONOMIC OVERVIEW

What a difference a quarter makes! Following the massive job losses Colorado experienced starting in February—the state shed over 342,000 positions between February and April—the turnaround has been palpable. Through August, Colorado has recovered 178,000 of the jobs lost due to COVID-19, adding 107,500 jobs over the past three months, an increase of 4.2%. All regions saw a significant number of jobs returning. The most prominent was in the Denver metropolitan service area (MSA), where 78,800 jobs returned in the quarter.

Although employment in all markets is recovering, there is still a way to go to get back to pre-pandemic employment levels. The recovery in jobs has naturally led the unemployment rate to drop: the state is now at a respectable 6.7%, down from a peak of 12.2%. Regionally, all areas continue to see their unemployment rates contract. I would note that the Fort Collins and Boulder MSA unemployment rates are now below 6%. Cases of COVID-19 continue to rise, which is troubling, but rising rates have only slowed—not stopped—the economic recovery. Moreover, it has had no noticeable impact on the state’s housing market.

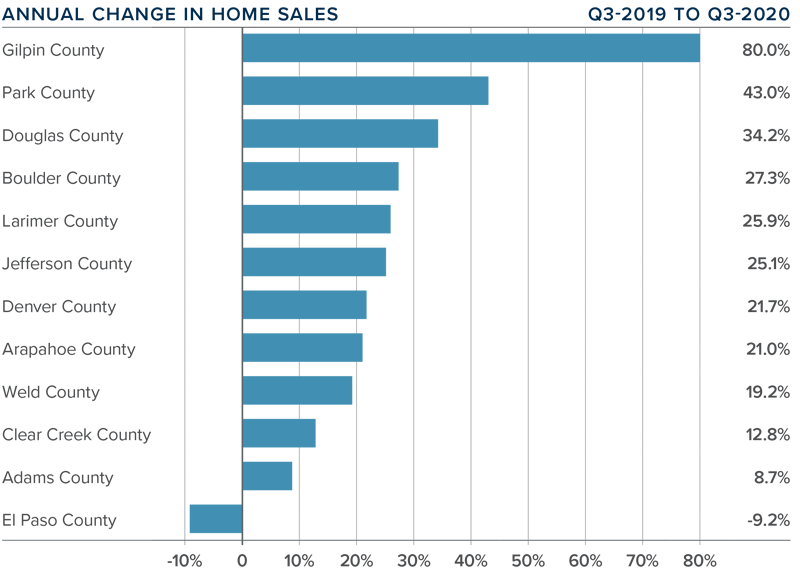

HOME SALES

- In the third quarter of 2020, 15,065 homes sold. This represents an increase of 20.4% over the third quarter of 2019, and a remarkable 52.7% increase over the second quarter of this year.

- Home sales rose in all markets other than El Paso compared to the second quarter of 2019. I believe sales are only limited by the number of homes on the market.

- Inventory levels remain remarkably low, with the average number of homes for sale down 44.5% from the same period in 2019. Listing activity was 17.8% lower than in the second quarter of 2020.

- Even given the relative lack of inventory, pending sales rose 17.8% from the second quarter, suggesting that closings for the final quarter of the year will be positive.

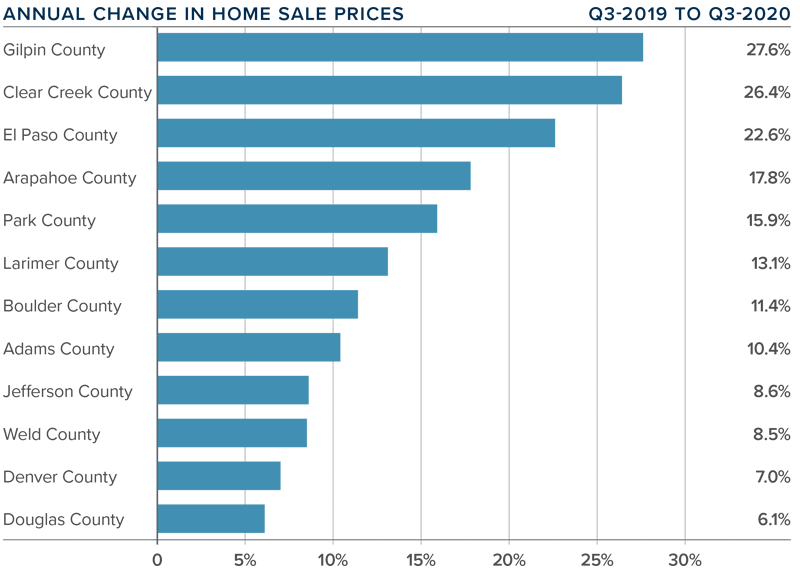

HOME PRICES

- After taking a pause in the second quarter, home prices rose significantly in the third quarter, with prices up 11.9% year-over

-year to an average of $523,193. Prices were up 7.4% compared to the second quarter of this year.

-year to an average of $523,193. Prices were up 7.4% compared to the second quarter of this year. - Interest rates have been dropping. Although I do not see there being room for them to drop much further, they are unlikely to rise significantly. This is allowing prices to rise at above-average rates.

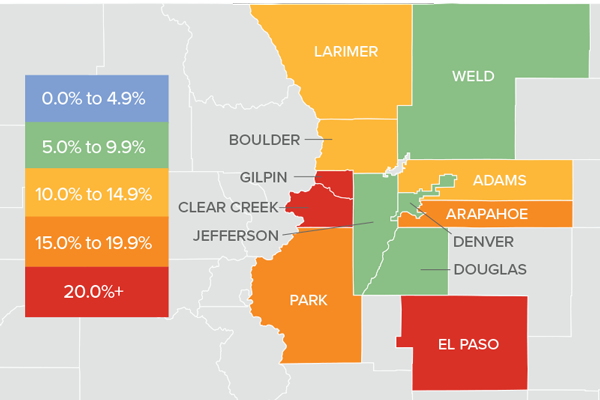

- Year-over-year, prices rose across all markets covered by this report. El Paso, Clear Creek, and Gilpin counties saw significant price appreciation. All but four counties saw double-digit price gains.

- Affordability in many Colorado markets remains a concern, as prices are rising at a faster pace than mortgage rates have been dropping.

-year to an average of $523,193. Prices were up 7.4% compared to the second quarter of this year.

-year to an average of $523,193. Prices were up 7.4% compared to the second quarter of this year.

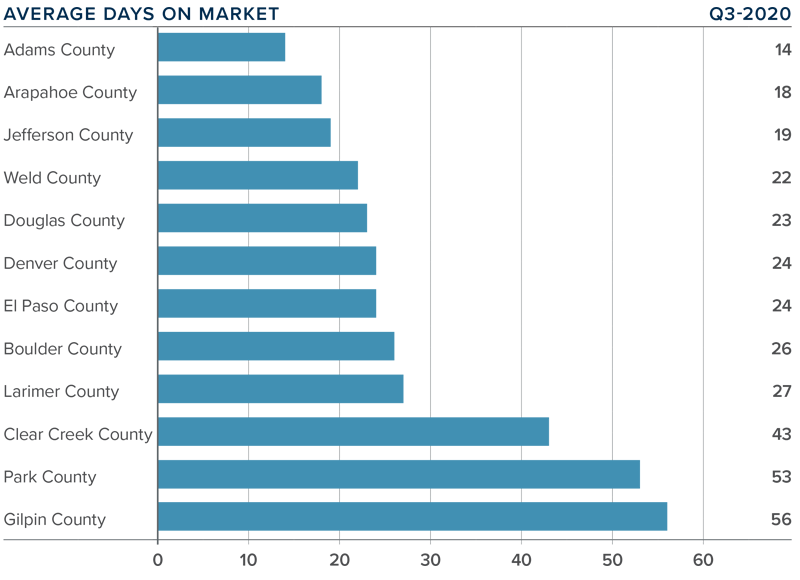

DAYS ON MARKET

- The average number of days it took to sell a home in the markets contained in this report dropped one day compared to the third quarter of 2019.

- The amount of time it took to sell a home dropped in nine counties, remained static in two, and rose in one compared to the third quarter of 2019.

- It took an average of 29 days to sell a home in the region.

- The Colorado housing market continues to demonstrate solid demand, and the short length of time it takes to sell a home suggests buyers are competing fiercely for available inventory.

CONCLUSIONS

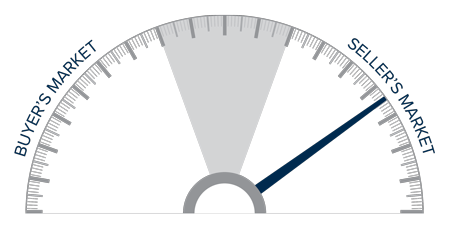

This speedometer reflects the state of the region’s real estate market using housing inventory, price gains, home sales, interest rates, and larger economic factors.

This speedometer reflects the state of the region’s real estate market using housing inventory, price gains, home sales, interest rates, and larger economic factors.

Demand for housing is significant, and sales activity is only limited by the lack of available homes to buy. Prices are rising on the back of very competitive mortgage rates and a job market in recovery. I suggested in my second-quarter report that the area would experience a “brisk summer housing market” and my forecast was accurate. As such, I have moved the needle a little more in favor of home sellers.

ABOUT MATTHEW GARDNER

As Chief Economist for Windermere Real Estate, Matthew Gardner is responsible for analyzing and interpreting economic data and its impact on the real estate market on both a local and national level. Matthew has over 30 years of professional experience both in the U.S. and U.K.

As Chief Economist for Windermere Real Estate, Matthew Gardner is responsible for analyzing and interpreting economic data and its impact on the real estate market on both a local and national level. Matthew has over 30 years of professional experience both in the U.S. and U.K.

In addition to his day-to-day responsibilities, Matthew sits on the Washington State Governors Council of Economic Advisors; chairs the Board of Trustees at the Washington Center for Real Estate Research at the University of Washington; and is an Advisory Board Member at the Runstad Center for Real Estate Studies at the University of Washington where he also lectures in real estate economics.

Economic Update with Matthew Gardner

Exclusive Invitation!!!

Tune in on Tuesday, October 6, 2020 at 9:00am to meet with Matthew Gardner, Windermere Real Estate’s Chief Economist LIVE and get your chance to ask him questions. He’ll be discussing the housing market, employment and the effects of COVID-19 on the local and national economy.

As one of the only real estate companies in the US that has a Chief Economist on staff, we have exclusive insights into the housing market, economy and government happenings. This is a one of a kind event for clients and friends of Windermere Real Estate in Colorado.

To sign up, please contact your Windermere Agent or message us to get the link. Seating is limited in digital meeting room so get your seat!

(If you can’t attend live, you can register to automatically get the recording.)

Matthew Gardner Weekly COVID-19 Housing & Economic Update: 5/11/2020

Job growth is critical to the health of the housing market, so on this week’s episode of “Mondays with Matthew,” Windermere Chief Economist Matthew Gardner analyzes the effect of COVID-19 on employment and what we can expect for the duration of the year.

Why So Many Americans Are Either Upsizing or Downsizing

Posted in Buying, Selling, and Living by Shelley Rossi

According to two recent surveys that took industry watchers by surprise, many family homeowners are putting frugality aside and upsizing to new houses that average as large as 2,480 square feet (an increase of as much as 13 percent from the year before), and sometimes exceed 3,500 square feet in size.

Meanwhile, millions of baby boomer homeowners are rushing to downsize—with some 40 percent of Americans between the ages of 50 and 64 saying they’re planning to make a move within the next five years.

It’s a tale of two very different segments of the population making dramatic shifts in their living accommodations to find the housing solutions that best suit their needs: one upsizing while the other downsizes.

With so many baby boomers now nearing retirement age (8,000 Americans turn 65 every day), it should come as no surprise that the number of prospective “downsizers” exceed the number of “upsizers” by three to one. With their children gone, these aging homeowners are interested in reducing the amount of house they need to care for, and are eager to bulk up their retirement savings with any home-sale profits.

As for why many families are choosing to upsize so substantially after years of downsizing or staying put, experts point to the extremely low interest rates and discounted home prices available today, and theorize that many families now feel confident enough about the economy to move out of homes they outgrew years ago.

If you’re considering upsizing or downsizing, here are some facts to consider:

How such a move can impact your life

The most common benefits of downsizing:

- Lower mortgage payments

- Lower tax bills

- Lower utility bills

- Less maintenance (and lower maintenance expenses)

- More time/money for travel, hobbies, etc.

- More money to put toward retirement, debts, etc. (the profits from selling your current home)

The most common benefits of upsizing

- More living space

- More storage space

- More yard/garden space

- More room for entertaining/hosting friends and family

Negative impacts:

- Upsizing will likely increase your living expenses, so it’s important to factor into any financial forecasts

- Downsizing will require that you make some hard choices about what belongings will need to be stored or sold

Other impacts to consider:

- The loss of good neighbors

- Lifestyle changes (walking, neighborhood shopping, etc.)

- The effect on your work commute

- Public transit options

Buy first, or sell first?

Homeowners considering this transition almost always have the same initial question: “Should I buy the new home now, or wait and sell my current place first?” The answer is dependent on your personal circumstances. However, experts generally recommend selling first.

Selling your current home before buying a new one could mean you have to move to temporary quarters for some period of time—or rush to buy a new home. That could prove stressful and upsetting. However, if you instead buy first, you could be stuck with two mortgages, plus double property tax and insurance payments, which could quickly add up to lasting financial troubles.

If you need to sell in order to qualify for a loan, there’s no choice: You’ll have to sell first.

Another option:

You could make the purchase of the new house contingent on selling your current home. However, this approach can put you in a weak bargaining position with the seller (if you can even find a seller willing to seriously consider a contingency offer). Plus, you may be forced to accept a low-ball offer for your current house in order to sell it in time to meet the contingency agreement timing.

The truth is, most home sales tend to take longer than the owners imagine, so it’s almost always best to finalize the sale, and do whatever is necessary to reap the biggest profit, before embarking on the purchase of your new home.

When to make the transition

Ideally, when you’re selling your home, you want to wait until the demand from potential buyers is high (to maximize your selling price). But in this case, because you’re also buying, you’ll also want to take advantage of any discounted interest rates and reduced home prices (both of which will fade away as the demand for homes grows).

How will you know when the timing is right to both sell and buy? Ask an industry expert: your real estate agent. As someone who has their finger on the pulse of the housing market every day, they can help you evaluate the current market and try to predict what changes could be coming in the near future.

Even if you’ve been through it before, the act of upsizing or downsizing can be complex. For tips, as well as answers to any questions, contact a Windermere agent any time.